- Author: Raymond

- Category: Electric Vehicles Insurance

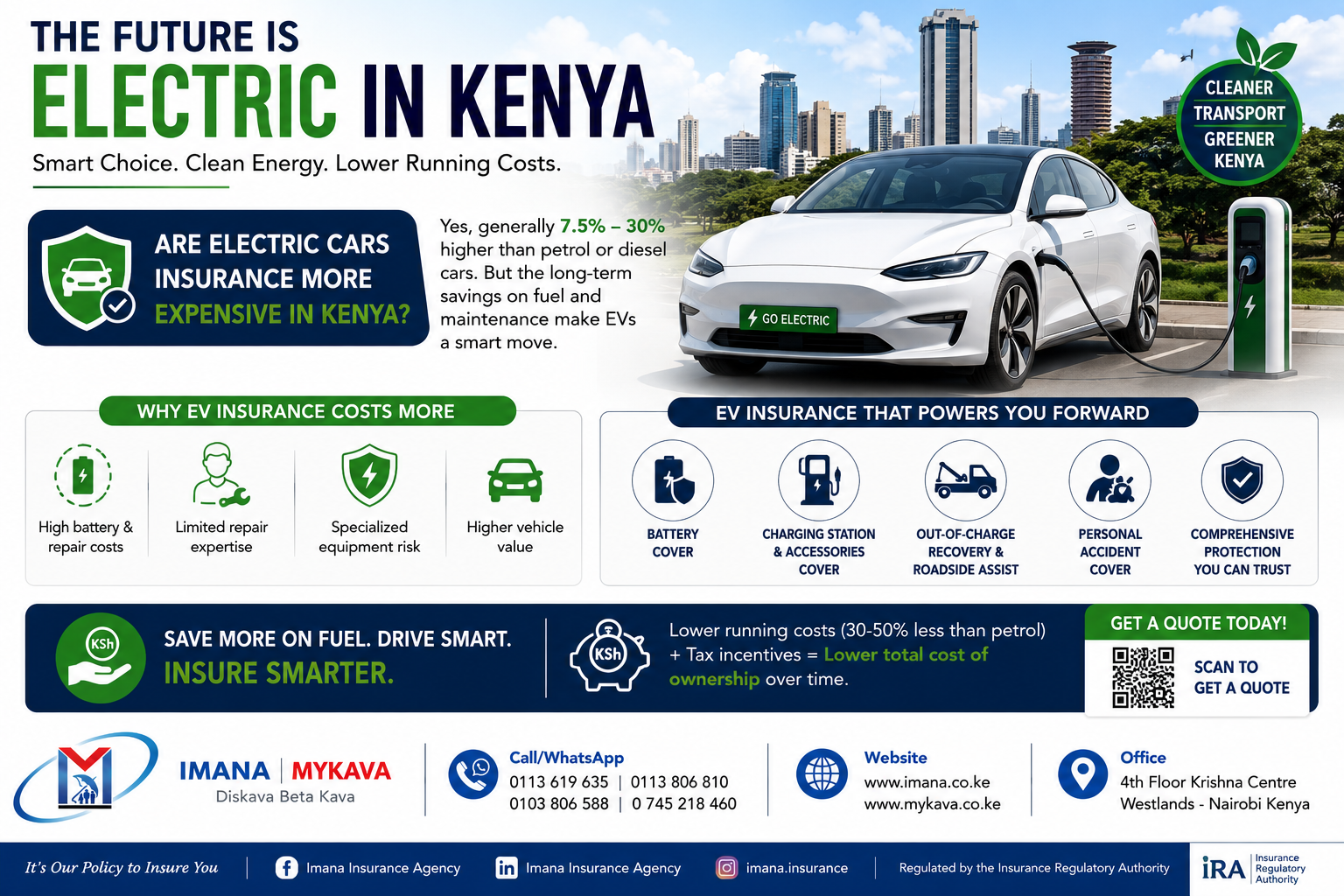

Are Electric Cars Insurance More Expensive in Kenya?

A Practical Guide for Kenyan EV Owners, Buyers & Businesses

Electric vehicles are no longer a “future thing” in Kenya. They are already here — from electric motorcycles and buses to private EVs, hybrid cars, delivery fleets and ride-hailing vehicles. Nairobi is slowly changing. The sound of the engine is getting quieter, but the insurance conversation is getting louder.

And the big question is simple:

Are electric cars more expensive to insure in Kenya?

The honest answer is yes — in many cases, EV insurance can cost more than insurance for petrol or diesel vehicles. The reason is not because insurers want to punish EV owners. It is because EVs carry a different type of risk: expensive batteries, specialized repairs, limited local expertise, charging equipment, and higher replacement costs.

Kenya’s EV market is also still young. Government policy is pushing e-mobility through tax incentives, EV infrastructure support, and a national electric mobility agenda, but the insurance market is still learning how to price this new class of motor risk. Kenya’s National Electric Mobility Policy includes measures such as tax exemptions for EV imports, charging infrastructure investment, and pilot projects for electric public transport.

First, Let’s Be Real: Why Are Kenyans Considering EVs?

Before we talk about insurance, ask yourself this:

Would you buy an electric car today if charging was easy, repairs were available, and insurance was affordable?

Many Kenyans are starting to look at EVs because fuel prices have become a headache. For boda operators, delivery businesses, taxi owners, fleet managers and private motorists, fuel is not just a cost — it is a daily wound.

EVs promise:

- Lower running costs

- Less dependence on petrol and diesel

- Reduced maintenance compared to traditional engines

- Cleaner urban transport

- Possible long-term savings

- Better fit for delivery, ride-hailing and predictable city routes

But here is where reality enters the room: buying the EV is one thing; insuring, repairing and maintaining it properly is another.

A petrol car mechanic is easy to find in Nairobi, Thika, Nakuru, Mombasa or Kisumu. EV technicians? Not yet everywhere. Spare parts? Not always easy. Battery replacement? That one can humble your bank account quickly.

That is why insurance matters.

So, Is EV Insurance More Expensive in Kenya?

Generally, yes. Electric vehicle insurance in Kenya is likely to be more expensive than normal motor insurance, especially for comprehensive cover.

In many markets, EV insurance premiums tend to be higher because EVs have expensive components and specialized repair needs. In Kenya, this is made more complicated by the still-growing repair ecosystem and limited historical claims data. Britam, for example, noted that EV owners face unique challenges such as high battery costs and limited repair infrastructure when launching its EV insurance cover in Kenya.

Some market estimates place EV insurance premiums at around 7.5% to 30% higher than comparable internal combustion engine vehicles, depending on the vehicle model, value, insurer, use, battery risk and repair availability. The exact figure will vary, so the smart move is not to guess — it is to compare quotes before buying.

You can request a motor insurance quotation through Imana Motor Insurance or compare cover options through Imana Insurance Agency Kenya Ltd.

Why EV Insurance Costs More in Kenya

1. The Battery Is Not Just a Battery — It Is the Heart of the Vehicle

In a petrol car, the engine is the big-ticket item. In an electric car, the battery and electric motor system are among the most expensive components.

That means even a moderate accident can become expensive if the battery pack, battery casing, electronic control unit, sensors or charging system is affected.

Pioneer’s EV Care product specifically includes battery and charging accessories coverage, showing how central the battery is to EV insurance design.

So when an insurer looks at an EV, they are not just asking:

“What is the market value of the car?”

They are also asking:

“What happens if the battery is damaged?”

“Can it be repaired locally?”

“How much will replacement cost?”

“Who is qualified to inspect it?”

That is where premiums start rising.

2. EV Repairs Require Specialized Skills

A normal garage may repair bumpers, doors, lights, windscreens and suspension. But EVs bring high-voltage systems, battery diagnostics, software, sensors and specialized safety procedures.

That means fewer approved repairers. Fewer repairers usually mean higher repair costs and longer repair timelines.

For insurers, that creates a problem: when repair costs are unpredictable, premiums become cautious.

Think of it this way:

A petrol car accident may need panel beating.

An EV accident may need panel beating, software checks, battery diagnostics and specialized electrical inspection.

Same accident. Different cost story.

3. Limited Local Claims Data

Traditional motor insurance in Kenya has decades of data. Insurers know how private cars, commercial vehicles, PSV taxis, matatus, pickups, trucks and motorcycles behave on the road.

EVs are different. The market is still developing. Claims data is still young. Repair networks are still forming. Battery performance in Kenyan conditions is still being studied.

When insurers do not have enough data, they price risk carefully.

That does not mean EV insurance will remain expensive forever. As more EVs enter the market, insurers will collect better data, repair networks will improve, and pricing should become more competitive.

4. Charging Equipment Adds a New Risk

With petrol cars, your “fueling equipment” is at the petrol station.

With EVs, part of the charging setup may be at home, office, depot, apartment basement, mall, business premises or fleet yard.

That raises new questions:

- Is the charger insured?

- What happens if charging equipment is damaged?

- Is the private charging station covered?

- What if there is electrical damage?

- What if the vehicle runs out of charge far from a charging point?

Modern EV insurance products are beginning to address this. Britam’s EV cover includes personal charging equipment and out-of-charge recovery to tow a stranded EV to the nearest charging station.

Pioneer’s EV Care also highlights emergency support, battery protection and charging accessories coverage.

This is the future of motor insurance: not just covering the car, but covering the ecosystem around the car.

What Should an EV Owner in Kenya Look for in Insurance?

Do not buy EV insurance the same way people buy normal third-party cover in a hurry.

Before you pay, ask the insurer or intermediary these questions:

Does the policy cover the battery?

This is the biggest one. Do not assume battery damage is automatically covered.

Does it cover the electric motor system?

The motor system is one of the most important components of the EV.

Does it cover charging accessories?

Ask whether home or private charging equipment is included.

Is out-of-charge towing covered?

This matters if you travel outside Nairobi or operate a commercial EV.

Are there approved EV repair garages?

A policy is only as useful as the claims network behind it.

Does the cover include theft, fire, accident damage and third-party liability?

Comprehensive EV insurance should still handle the basics.

Can I add Political Violence & Terrorism, Excess Protector, Courtesy Car or Road Rescue?

These add-ons matter, especially for private, business and fleet owners.

For help comparing motor insurance options, visit Imana Car Insurance in Kenya or request a quote through Imana Micro Quote.

Comprehensive vs Third Party for Electric Cars

Let’s keep it very practical.

If you own a low-value old petrol car, some people may choose Third Party Only because they are mainly trying to meet the legal requirement.

But for an EV, especially a newer or high-value one, Third Party Only may be too thin.

Third Party Only generally protects you against legal liability to other people — injuries, death or property damage. It does not repair your own vehicle.

Now imagine your EV is involved in an accident and the battery system is affected. If you only have Third Party Only, the cost of repairing your own EV may sit fully on your shoulders.

That is why EV owners should seriously consider Comprehensive Motor Insurance.

Comprehensive cover may help with:

- Accidental damage

- Theft

- Fire

- Third-party liability

- Battery-related extensions, where available

- Charging equipment extensions, where available

- Road rescue

- Courtesy car, depending on insurer terms

- Personal accident, depending on package

- Political violence and terrorism, if added

For guidance on comprehensive motor cover, you can visit Imana Motor Insurance.

Are EVs Still Worth It If Insurance Costs More?

This is where the conversation becomes interesting.

EV insurance may cost more, yes. But total ownership cost is not only about insurance.

You must look at:

- Fuel savings

- Maintenance savings

- Tax incentives

- Charging costs

- Battery warranty

- Resale value

- Insurance premium

- Repair access

- Business use

- Daily mileage

Kenya has been introducing measures to support electric mobility, including reduced excise duty rates for EVs, targeted tax exemptions and relief measures, and reduced electricity tariffs for EV charging.

The government has also announced new tax incentives, including exemptions from VAT and excise duties on EV parts and charging stations beginning July 2026, plus reduced stamp duty for EV infrastructure developments by 2027.

So yes, EV insurance may be higher today, but if your fuel and maintenance savings are strong enough, the overall cost can still make sense.

The best EV buyer is not the one who follows hype. It is the one who calculates.

Practical Scenario: Should a Nairobi Driver Buy an EV?

Let’s say you live in Ruaka and work in Westlands. You drive daily through Limuru Road, Waiyaki Way or Red Hill Road. You mostly operate within Nairobi, with occasional trips to Kiambu, Thika or Naivasha.

An EV could make sense if:

- You have reliable charging at home or work

- Your daily mileage is predictable

- You do not regularly travel to areas with limited charging access

- You understand battery warranty terms

- You can access qualified EV repair support

- You can afford comprehensive insurance

- You compare quotes before buying

But if you travel long-distance often, lack charging access, or depend on garages that do not handle EVs, you need to pause and plan properly.

EV ownership is not bad. Unplanned EV ownership is the problem.

For Businesses: EVs Can Be Smart, But Insure Them Properly

EVs may be a strong fit for:

- Delivery companies

- Courier businesses

- Ride-hailing fleets

- Office transport

- Corporate fleets

- Hotels and airport transfer businesses

- NGOs and institutions

- Security patrol fleets

- Urban logistics businesses

- Electric motorcycle operators

Why? Because businesses can calculate routes, charging times, maintenance schedules and operating costs more clearly.

But businesses must avoid one dangerous mistake:

Do not buy EVs as assets and insure them like ordinary petrol vehicles without checking the special risks.

A company EV fleet should consider:

- Comprehensive motor insurance

- Battery cover

- Charging equipment cover

- Road rescue

- Driver personal accident

- Fleet tracking

- Approved repair network

- Workplace charging safety

- WIBA/GPA for employees, where applicable

- Public liability if charging points are accessed by third parties

For business insurance guidance, visit Imana Corporate Quote or Imana Contact Us.

The Kenyan EV Insurance Market Is Starting to Wake Up

This is the good news.

Kenyan insurers are no longer treating EVs as strange machines from another planet. EV-specific covers are beginning to appear.

Pioneer Insurance launched EV Care, a comprehensive motor insurance product for electric motor vehicles, including electric cars, motorbikes and buses, with battery and charging accessories coverage.

Britam also launched EV insurance in Kenya for fully electric and hybrid vehicles, with battery protect cover, personal charging equipment cover and out-of-charge recovery.

This matters because once insurers begin competing in a category, products usually improve. Benefits become clearer. Pricing becomes sharper. Claims handling becomes more specialized.

The market is not perfect yet, but it is moving.

Before You Buy an Electric Car in Kenya, Do This Checklist

Use this before signing that sale agreement.

Check the battery warranty.

Ask how many years or kilometres are covered.

Confirm local repair support.

Do not rely on “we can import parts” as your only comfort.

Ask for insurance quotes before buying.

Do not buy first and panic later.

Confirm charging options.

Home, office, public charging and emergency charging all matter.

Understand range realistically.

Do not only trust brochure range. Ask how the vehicle performs in traffic, hills, heat and real Kenyan driving.

Check resale market.

EV resale is still developing in Kenya.

Ask whether the insurer covers the battery separately.

This should be very clear in writing.

Use a trusted intermediary.

A good insurance intermediary helps you compare, ask the hard questions and avoid weak cover.

You can start with Imana Motor Insurance or request help through Imana Contact Us.

What Documents Do You Need to Insure an EV in Kenya?

Most insurers will typically require the normal motor insurance documents, plus extra details depending on the insurer and vehicle type.

Prepare:

- Copy of logbook

- Copy of ID or passport

- KRA PIN

- Vehicle valuation report, especially for comprehensive cover

- Battery details, where requested

- Use of vehicle: private, commercial, fleet, delivery, taxi or institutional

- Existing policy details, if renewing

For comprehensive cover, valuation is especially important because EV values and battery values need proper documentation.

What Happens If Your EV Is Involved in an Accident?

Do not panic. Follow the normal accident process, but with EV-specific caution.

First, make sure everyone is safe. Then report the accident to the police where required. Take clear photos of the scene, vehicle damage, road position, registration numbers and any third-party property damage.

Then contact your insurer or intermediary immediately.

For EVs, do not allow unqualified people to tamper with the battery, charging port, underbody or electrical system. Even if the car looks okay, the battery and high-voltage system may need inspection.

This is where working with an intermediary like Imana helps. You need someone who can guide you on documentation, claim reporting, garage approval and insurer communication.

Will EV Insurance Become Cheaper in Kenya?

Most likely, yes — but not overnight.

EV insurance should become more competitive as:

- More EVs enter Kenyan roads

- More insurers create EV-specific products

- Garages develop EV repair capacity

- Spare parts become easier to source

- Battery diagnostics improve

- Claims data becomes more reliable

- Charging infrastructure grows

- Government incentives reduce EV ecosystem costs

Kenya’s EV numbers are growing, especially through electric motorcycles, buses and fleet vehicles, and policy support is pushing the market forward.

But for now, buyers should remain realistic. EVs are promising, but insurance needs careful planning.

EV Wisdom: EVs Are the Future, But Don’t Buy the Future Blindly

Electric vehicles are coming into Kenya with a quiet confidence. No roaring engine. No petrol station stress. No exhaust smoke drama. Just a new way of moving.

But insurance is where the dream meets paperwork.

So before you buy that electric car, ask the right questions. Compare cover. Understand battery protection. Confirm charging equipment cover. Check repair networks. Look beyond the premium and read the policy benefits.

Because the cheapest insurance is not always the smartest insurance.

At Imana Insurance Agency Kenya Ltd, we help individuals, families, businesses and fleet owners compare motor insurance options and choose practical cover based on real risk — not guesswork.

For EV, hybrid, petrol or diesel motor insurance guidance, visit:

Motor Insurance in Kenya

Imana Health Insurance

Corporate Insurance Quote

Request a Quick Quote

Contact Imana

Call/WhatsApp: +254 796 209 402

Office: 4th Floor, Krishna Centre, Woodvale Grove, Westlands, Nairobi

Website: www.imana.co.ke

#ElectricVehiclesKenya #EVInsuranceKenya #MotorInsuranceKenya #GreenMobilityKenya #ImanaInsurance